How can economic policy-makers use economic history as a guide for their deliberations and decisions? Focusing on the case of central banking, this essay argues that the virtue of history is not only to improve economic models and quantitative studies, but to provide a perspective distinct from standard economic reasoning.

Recherche

Télécharger l'article :

PDF

This essay was first written for the History and Policy Making Conference at the Bank of England, 30th November-December 1st. I thank the organizers for their invitation and participants for questions. Special thanks to David Aikman, Austen Sanders, Sophie Cras, Catherine Guesde, Nicolas Delalande for their detailed remarks. Austen Saunders’ blog post served as an insightful starting point for this conference and the present essay.

In the aftermath of the 2008-2009 financial crisis, students, journalists and policy-makers blamed economists’ lack of historical knowledge. Insufficient understanding of the past—it was said—would explain why the risk of financial instability remained under the radar. These criticisms led to some important initiatives (e.g. the Institute of New Economic Thinking and its “Young scholar initiative” etc.), numerous conferences, and they even fueled the success of some books and academic articles on financial history. Some central banks—especially the Bank of England through the voice of Andy Haldane, then Director of Financial Stability—explicitly acknowledged that insufficient historical thinking was detrimental to their role as financial supervisor and market stabilizer. [1]

Yet, such calls eventually had little effects on policy making, research, academic employment and teaching. The response of central banks to the 2008 crisis was justified by some references to the policy mistakes of the 1930s but, in other areas such as fiscal policy or sovereign debt, policymaking was hardly informed by any relevant historical perspective. In many instances, the sentence “learning the lessons from history” sounded like an empty claim without genuine historical substance. [2] Economic research and teaching in universities has not been revolutionized by an historical turn either. [3]

A remarkable change took place however: the tremendous effort of some central banks and international organizations (International Monetary Fund, Bank of International Settlements in particular) to build and publish online historical documents and statistical series and—more generally—to invest in historical research and the production and dissemination of historical resources. It seems that these initiatives were not only driven by a general trend towards archival digitization (or by the celebration of the anniversary of central banks…) but were also explicitly motivated by the belief that historical knowledge is key to policy making. [4]

Recognizing that less progress has been made on how to effectively articulate historical knowledge with policy making, the Bank of England (the United Kingdom’s central bank) recently gathered economic historians and policymakers to tackle this question. In my opinion (which I expressed at this conference), the starting point for addressing this issue is to ask what central bankers should expect from research in economic history that they would not find in other types of economic research. Central banks now have large research departments full of leading economists whose publications and influence equal those of academic economists. [5] More generally, these institutions and their top management are very closely connected to academic research. How does economic history research fit into this context?

The Tension between Economic and Historical Approaches

My contention is that economic history provides a third perspective to policy-making that is distinct from the perspectives offered by economic theory and empirical economics. In my experience, economists in academia and central banks often postulate that economic history is useful because it supplies historical cases to test economic theory, or because it provides longer data for empirical economic studies. In this view, history is subservient to theoretical and applied economics. If true, the contribution of historical research to policy making is valuable but only indirect. I would argue, on the contrary, that a historical perspective also makes a direct contribution to economic policy making because thinking historically provides insights that are different from the ones that standard economic thinking has to offer. In other words, economic history provides economists and policy-makers not only with objects and data, but also with a distinct methodology and epistemology.

In a recent essay on historical perspectives on contemporary challenges to globalization, the economic historian Kevin O’Rourke wrote:

As economists, we are trained to look for patterns and to seek general explanations for entire classes of phenomena rather than specific explanations for individual historical events. But as historians we are trained to recognize the uniqueness of individual events and acknowledge the roles played in them by context, contingency, and the choices made by individual actors. [6]

This sentence reveals very well the tension that inhabits the work of economic historians today. This tension continues to grow as the discipline of economics seeks to imitate the natural sciences and essentially values studies that aimed to reveal some general laws of the world. Thus, most economists and economic policy makers have been trained to disregard contributions that emphasize the singularity of past and current events. Taking the laboratory experiments of medical sciences as a gold standard, they search for “external validity”. In this view, history is only useful to policy-making if it helps economists to generalize and draw clear policy lessons from past events.

Taking the opposite side, I argue that understanding why the present is different from the past is insightful for policy-making because it helps identify today’s salient features on which policy-makers should and can act. What is fascinating about history is its otherness. When historians shed a long-term perspective on a topic, showing how the present is shaped by history, it is not to offer a deterministic view of historical evolution or reveal the inability of human nature to change. The purpose is to emphasize how the current situation is a unique product of historical trends and contingent forces. In the current context of uncertainty and profound economic transformations, the historical viewpoint can also help to think of those moments of bifurcation, when intellectual and political models are redefined (thus avoiding naturalizing economic outcomes).

As examples, I will discuss below how economic history can contribute to the debates on macroprudential policy (that is controlling credit to ensure financial stability) and—more suggestively—on the holding of public debt by the central bank. [7] This will lead me to conclude briefly on how to articulate economic history research with the public service of providing better access to archival data and long-term statistical series (i.e. historical resources). [8]

The Theoretical and Empirical Perspectives, and how Economic History Contributes to Them

Think about a policy maker who wonders whether it is desirable to control credit to prevent the occurrence of banking crises and, if so, how to implement this kind of controls. This is what is now called macroprudential policy. Although it is sometimes implemented by central banks, it is different from monetary policy. It is also different from banking regulation (named “microprudential”) whose goal is to protect depositors and avoid the failures of individual institutions. Macroprudential policy follows a systemic approach; it aims at using banking or financial regulation to act on the quantity of credit granted by some targeted institutions or to some targeted borrowers. [9]

Rather than relying on her own judgment or on advices from the financial sector, the policy maker is looking for some expertise by research economists. She probably already knows that she will obtain as many answers and points of view as the number of economists in the room, but she is also convinced that the exposition of different arguments will help her understand better what is at stakes.

Economic theory provides powerful tools to justify a policy intervention by identifying the market failure. It also pins down how macroprudential tools can be substitute or complementary with other policy instruments. [10] Applied economics provides a second and complementary perspective. Using either reduced form estimations or macroeconomic modelling, it is essential to test economic theory (and so the claims justifying policy intervention) and assess the expected effects of a policy measure. Since the first implementations of macroprudential measures, a large number of studies measure their effects, relying on standard tools of policy evaluation applied in other domains. Before that, Borio & Drehmann and Schularick & Taylor provided empirical evidence on how credit booms lead to banking crises. [11] Macroeconomic models can, in addition, be used to simulate the effect of the measures, considering parameters that are more specific to the economy or instruments under scrutiny.

Economic history can inform the theoretical and empirical perspectives on macroprudential policy. For example, Miklos Vari and I have shown that liquidity ratios similar to the current Liquidity coverage ratio (LCR) were widely used in the past by central banks and we built a model to reproduce the theoretical mechanisms underlying these historical policies. [12] Although the context is obviously different, the same theoretical mechanisms might be at work today. As such, history works as a giant tool box where economists can pick interesting cases to improve their toy models. The same holds true for empirical economics. The work of Moritz Schularick & Alan Taylor on the link between credit booms and banking crisis relies on 150 years of data. They argue that such a long-term perspective is essential since crises are rare events. There is also a large literature using some historical episodes to test economic models, relying either on time series or on comparative case-studies (“natural experiments”) to check whether historical patterns fit theoretical predictions. [13] Last, finding some historical precedents may provide opportunities to assess the potential effects of actions foreseen by current policy makers. In this vein, a body of work thus draws an analogy between some forms of credit controls by central banks in the past, and the current proposed form of credit controls (named macroprudential). [14] If one believes that there are enough similarities between current macroprudential measures and their historical precedents, the results from these studies can guide the implementation of today’s policy. The standard theoretical and empirical approaches in economics aim at generalizing arguments and results. Along these two perspectives, the peculiarities of the historical period under study are perceived to be a weakness of the analysis because they may undermine the “external validity” of the research design.

Economic History as a Third Perspective for Policy-Making

If the two perspectives presented above (theory and empirics) can make a direct contribution to policy-making, and if history is a valuable input for these two approaches, then historical research makes an only indirect contribution to policy making. I now turn to the argument that economic history has a distinct and direct perspective to offer.

The historical perspective acknowledges and values the uniqueness of historical periods and of the current context. Regarding debates on macroprudential policy, this perspective highlights that credit controls in history were in fact used mostly for monetary policy purposes (fight inflation, stabilize the exchange rate) rather than for financial stability. [15] Monetary and credit policy were conflated (which does not imply that different instruments had the same effects). Why is it useful to recognize that the same policy instruments (limits to credit growth) were used in the past with a different purpose from those given to them today? It forces us to think on what macroprudential policies are really about. The lessons from history are not straightforward and the past experiences of central bank with credit controls can be interpreted in different ways, they may help to clarify the objectives and underlying motivations of current macroprudential policy.

The most striking feature of past credit controls in most countries was their distributive aspect. They were intended to achieve price and credit stability by giving priority to some sectors or financial institutions. Credit controls were eventually disregarded in the 1980s because of these distributive effects but, in the preceding decades, such effects were seen as an advantage. Acknowledging the distributive aspect of credit controls—and, more generally, central bank credit policies based on the choice of collateral—might lead current policymakers to worry that macroprudential policy is at odds with central bank independence. On the contrary, some would conclude from the historical experience that the period that spans from the early 1990s to 2008 was an exception, and that credit policy should become a backbone of central banking again.

Recognizing the singularity of the past should not prevent analogies with the current period, nor hypotheses about the way the past has shaped the present. [16] But, contrary to the standard perspective in empirical economics, the analogies and hypotheses should themselves be contextualized. We are not simply comparing two different policy experiments happening at the same time. The way we think about macroprudential policies today, and, most importantly, the reason we have to think about them today is itself the product of the past. Credit controls were repealed in the 1980-1990s because they were seen as an extremely complex systems creating rents in the banking systems and leading banks to take even more risk by trying to escape them. Yet, another reason for the abolishment of credit controls was an unfettered belief in the self-regulation of financial markets. And it is unlikely that we can justify macroprudential policy without overturning (at least partly) this belief. The historical perspective thus helps to reframe the debate on the rationale and institutionalization of macroprudential policy. The issue is not so much if and how macroprudential credit controls might work, but how they can be justified in light of the historical experience of central banks with the control of credit.

Another output of putting macroprudential policy in its historical context might be to shed a skeptic light on the recent fashion to relabel many monetary tools—especially used in low-income countries (“emerging markets”)—as macroprudential tools. In most cases, the relabeling does not really corresponds to the actual use since these countries are still using banking regulation tools for monetary policy, especially when money markets are not mature enough to transmit fully central bank actions to the whole economy. It would be better to treat them as such, rather than to reinterpret monetary policy tools in emerging markets through the eyes of the current US and European experiences.

Taking into account the singularity of historical episodes may also push us to go beyond the average effects observed in empirical studies. Michael Bordo uses historical evidence to cast doubt on the fact that credit booms are a leading indicator of financial crises in general. [17] No one factor dominates across all countries and time and, he argues, it is very important for policy making to recognize first and foremost that financial crises are extremely heterogeneous and rare events. Otherwise, the risk is to try to anticipate a crisis that resembles the previous one, instead of understanding the singularity of current imbalances.

It is remarkable that the same body of work on the history of credit policies (see references in footnote n°13) can provide insights for policy-making either through the empirical perspective or through the historical perspective. On one hand, this kind of work aims to provide some general arguments on the effectiveness of credit controls and macroprudential policy. On the other hand, it emphasizes the uniqueness of the past and thus—as a counterpart—the salient features of the present. As reminded by Kevin O’Rourke in the quote above, many studies in economic history offer such a dual perspective and thus can in fact be read from different angles. The influential work of Moritz Schularick and Alan Taylor provides a general statement about the average consequences of credit booms over more than a century, but it also puts the current period in its peculiar context by emphasizing that never before the ratio of credit to GDP has been so disconnected from the ratio of money to GDP (what they call the “Great Leveraging”). [18] In other words, bank lending is no longer primarily financed by bank deposits, but by short-term funding from financial markets. This is a major change due to financial liberalization and globalization of the 1980s, without equivalent, even during the first era of globalization before the First World War.

This is one of the key reasons why, as argued by Adam Tooze, the international financial contagion during the 2008-2009 crash was very different from the one of the Great Depression of the 1930s. [19] The understanding of such major historical shifts is key to fully grasp the stakes of macroprudential stability today. Yet, such historical perspective may also question whether macroprudential policy and liquidity regulation are enough to minimize financial risk and reduce financial leverage in a world where the international money market plays such a key role in maturity transformation.

Looking at the historical evolution of credit cycles, rather than bank leverage, offers a somewhat different view however. In our investigation of world financial and real cycles, we provide some descriptions of the average patterns of these cycles since 1950: the strength of the global factor of asset prices has strongly increased since the wave of financial liberalization in the 1980s but it is not the case for global bank credit cycles, despite the Great Leveraging. [20] With the exception of the 2008-2009 disruption in the global money market, credit cycles are still much more determined by idiosyncratic domestic factors than by a world component. The historical evolution of credit and asset cycles have been different. Banking credit is still highly regulated in most countries and international connections of credit markets for households and firms are still limited, even without capital controls (think about housing credit for example). There is still some room for credit controls.

Public Debt and Central Banks

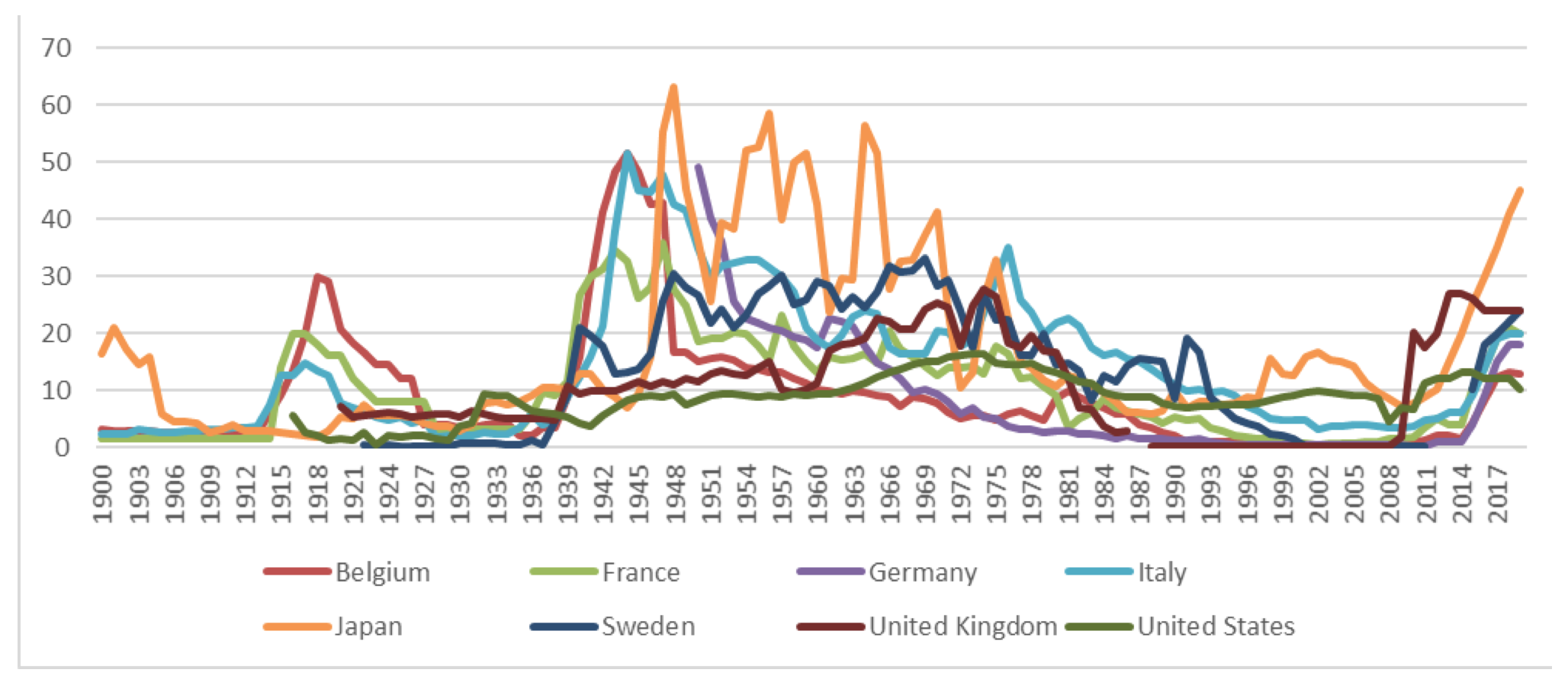

A key issue for policy-makers and central banks today—especially in Europe and Japan—is the surge in the share of public debt held by the central bank. Around 20% before the Covid-19 crisis in the Euro-area and England (and 40% in Japan), this share is now approaching 30% (above 50% in Japan in 2021). Such figures are not without historical precedents (see Figure 1). For sure, economic theory has a lot to say on the link between public debt and monetary policy and applied economists can also use series like the ones of Figure 1 to discuss the average relationship between public debt held by the central bank and several macroeconomic variables. By contrast, a historical perspective would highlight the singularity of our times. Figures 1 hides—at least—two interesting differences between the current holding of public debt by central banks and the one of the 1950-1970s (I exclude comparisons with war times).

First of all, public debt was much lower in the 1950s-1970s than it is today: the public debt ratio was on average a quarter of its current value. Hence the total size of public debt held by the central bank in proportion of national income was much smaller. Second—and most importantly—, the institutional and economic context was very different. History differs across countries (the US being a notable exception in this respect), but the norm of the postwar period was that central banks would lend directly to the State or purchase public debt on the primary market. The monetary financing of public debt was allowed but constrained by law, such that there could be some important political costs for a government to rely excessively on this kind of financing. [21] Moreover, increase in monetary financing was often inflationary so that—at least during the 1950s and 1960s—it often had to be counterweighted by restrictive monetary policy. Restrictive policy typically targeted private lending and aimed at maintaining the yield on public debt stable. Non-independent central banks could finance the government directly (i.e. at the government’s request) but this was not without constraints. Depending on the country, these two constraints (legal constraints and inflation) played different roles.

By contrast, these two constraints have disappeared in the current situation. Central banks are forbidden to finance public debt at the government’s request and only purchase government bills from banks on the secondary market. The purchase of public debt is much less explicitly integrated into the state apparatus, politically and economically. It has no direct effect on money creation and inflation, since the counterpart of the purchase of government debt is simply the accumulation of bank reserves at the central bank. This simple historical perspective emphasizes that the current situation is really unique and that—without a return of inflation—it seems that today’s accumulation of public debt by central bank is an almost unconstrained phenomenon. It is an irony of history and was certainly not foreseen by the promoters of central bank independence in the 1990s. Is there a need to institutionalize this new political situation and recognize that the legal mandate of central banks established in the 1990s does no longer fit with our times?

Would a return of inflation lead central banks to adopt the policies of the 1950s-1960s that gave priority to public debt financing over private credit during times of contractionary monetary policy? These are some questions raised by a historical perspective on the matter. [22]

Figure 1. Share (in %) of total public debt held by the central bank. 1900-2019

Sources : Abbas, S. A., Blattner, L., De Broeck, M., El-Ganainy, M. A., & Hu, M. (2014). Sovereign debt composition in advanced economies : a historical perspective (No. 14-162). International Monetary Fund. Updated (post 2012) with “Bruegel database of sovereign bond holdings (Update April 2020) developed in Merler and Pisani-Ferry (2012)”, central bank websites and with Monnet (2018) for French historical series.

Conclusion

Studies in economic history usually follow one of these two different methods: a long-term approach where the present appears as a unique combination of historical paths; a focus on a historical period, institution or events, to which the present can be compared. These two approaches highlight contingency and, accordingly, give a role to political agency. Contingency is also a way to think about alternatives, and thus adopt a skeptical approach on deterministic discourses. A historical approach is the best way to avoid the false and hubristic belief that lessons have been learned from history. In many instances, a prominent role of a historical approach is to debunk easy claims that state that “it has to be like this”. The use of history for policy-making thus inevitably relies on counterfactual reasonings, which becomes key to think about human and political agency: how could things have turned differently? How can they be different in the future? In this way, the insights of the historical approach to policy making are paradoxically not so different from the insights that economic theory has to offer Historical narratives and theoretical models are two excellent suppliers of counterfactuals.

I will conclude by suggesting how archives and historical research can be used in central banks, alongside the previous discussion. In my mind, it is necessary to distinguish and articulate three ways of investigating history in these institutions. Firstly, there is a requirement to provide a public service and thus to make archival data available to the public as extensively as possible. It can take different forms: easy access to primary sources (including through exhaustive inventories and digitization), contributions by in house or official historians, and datasets building. Secondly, the central bank can hire economic historians in the research department to exploit this archival information in ways that are directly consistent with policy questions. In my experience, economic history research is difficult to conduct on a large and innovative scale without sufficient investment by the central bank in the collection and provision of historical data. It does not mean that this investment should be done only in house, without external advising or cooperation, nor that economic historians working in a central bank should focus on the history of their own institution only. But it should be recognized that economic history research needs to rely on these resources. Thirdly, central banks—as other policy institutions—should temporarily organize some research projects on specific aspects of their history (economic or social), and appoint academic historians to undertake these projects. The external researchers should not be bound by any instructions with regard to the project’s content, and they should be a diverse group, in terms of research methods and interests. As for economic historians in the central bank’s research department, academic historians should benefit from the substantial investment of the central bank in the provision of primary qualitative and quantitative historical sources. Economic historians in academia and in central banks are not substitutes but complements.

Dossier's Articles

by , 8 February 2021

Find us here :

To quote this article :

Éric Monnet, « Why Central Bankers Should Read Economic History », Books and Ideas , 8 February 2021. ISSN : 2105-3030. URL : https://mail.laviedesidees.fr/Why-Central-Bankers-Should-Read-Economic-History

Nota Bene:

If you want to discuss this essay further, you can send a proposal to the editorial team (redaction at laviedesidees.fr). We will get back to you as soon as possible.

You might also like

Footnotes

[1] This context and such claims have been recently summarized in Austen Saunders, “Thinking Historically”, Bank Underground, 30 July 2020. The fact that some eminent experts on the Great Depression were key policy makers or advisers after the financial crisis also gave the impression that the time had come for financial and monetary economists to value historical expertise as much as statistical knowledge. Christina Romer became the chief of Council of Economic Advisors of Barack Obama. Frederic Mishkin and Ben Bernanke were governors of the Federal Reserve. See Eichengreen, B., Hall of Mirrors: The Great Depression, the Great Recession, and the Uses and Misuses of History, Oxford University Press, 2014. We can now add to this list Isabel Schnabel, who has recently joined the board of the European central bank.

[2] Barry Eichengreen and Adam Tooze have highlighted and analyzed these misuses. Eichengreen, B., Hall of Mirrors: The Great Depression, the Great Recession, and the Uses and Misuses of History, Oxford University Press, 2014. Tooze Adam, “History and America’s Great Recession”, Books and Ideas, 25 November 2013.

[3] There is a recent trend of papers published in general economic interest journals looking at the persistent effect of historical institutions or cultural traits on current economic outcomes. Seen from this perspective, economic history may be enjoying a new academic success. However, this kind of work interacts little with existing literature in economic history (see Cioni, M. , Giovanni F. and Vasta, M., “Three Different Tribes: How the Relationship between Economics and Economic History Has Evolved in the 21st Century”, CEPR Discussion Paper No. DP14192., 2019. Furthermore—and most important for this essay—it has no direct relevant implication for policy-making (and does not claim to have), and it has actually little influenced the field of financial and monetary economics (see Monnet, E., & Velde, F. R., “Money, Banking, and Old-School Historical Economics”, CEPR Discussion Papers no. 15348, 2020).

[4] The Bank of England and the Federal Reserve have been at the forefront, making a large volume of digitized documents and statistical series available online [URLs: https://www.bankofengland.co.uk/archive ; https://www.bankofengland.co.uk/statistics/research-datasets ; https://fraser.stlouisfed.org/].The BoE has also launched an extensive research program on Bank’s operations as lender of last resort during past financial crises. Some other central banks have been involved, especially as it corresponded to bicentenary. Academic have also contributed to this trend. See Monnet & Velde, op. cit, (2020) for a recent survey of publications in central bank history. At the Bank of England conference on December 1st2020, David Aikman also presented evidence that working papers published by research departments of central banks has sharply increased since 2008.

[5] Claveau, F., & Dion, J., “Quantifying Central Banks’ Scientization: Why and How to do a Quantified Organizational History of Economics”, Journal of Economic Methodology, 25(4), 2018, 349-366.

[6] O’Rourke, K. H., “Economic history and contemporary challenges to globalization”, The Journal of Economic History, 79(2), 2019, 356-382.

[7] The history of the international swap networks between central banks provides another recent example of insightful study for policy-making. The perspective of Catherine Schenk and Robert McCauley is similar to the one I defend here, highlighting the tension between historical similarities and differences, rather than trying to generalize outside of the historical context. McCauley, R. N., & Schenk, C. R., Central bank swaps then and now: swaps and dollar liquidity in the 1960s (No. 851), Bank for International Settlements, 2020.

[8] I discuss here the relationship between research and policymaking in the case of central banks but it is likely that my arguments could be more general and applied to other institutions responsible for economic policy (Ministries and international organizations in particular). I must also add that discussing the potential impact of research on policy does not imply that the value of research should be assessed primarily through its direct policy impact, especially in academia.

[9] For a review and presentation, see Aikman, D., Bridges, J., Kashyap, A., & Siegert, C., “Would Macroprudential Regulation Have Prevented the Last Crisis?, Journal of Economic Perspectives, 33(1), 2019, 107-30.

[10] As examples of these two respective contributions, see Farhi, E., & Werning, I., “A Theory of Macroprudential Policies in the Presence of Nominal Rigidities”, Econometrica, 84(5), 2016, 1645-1704.; Jeanne, O., “The Macroprudential Role of International Reserves”, American Economic Review, 106(5), 2016, 570-73.

[11] Borio, C. E., & Drehmann, M., “Assessing the Risk of Banking Crises”–revisited, BIS Quarterly Review, March, 2009. Schularick, M., & Taylor, A. M., “Credit Booms Gone Bust: Monetary Policy, Leverage Cycles, and Financial Crises, 1870-2008, American Economic Review, 102(2), 2012, 1029-61.

[12] Monnet, E., & Vari, M., A Dilemma Between Liquidity Regulation and Monetary Policy: Some History and Theory (No. 15001), CEPR Discussion Papers, 2020.

[13] See Monnet & Velde, Op. cit, (2020) for a recent—but of course incomplete—survey.

[14] French credit controls (1948-1973) had an impact on credit, output and inflation while keeping interest rate unchanged (Monnet, E., “Monetary Policy Without Interest Rates: Evidence from France’s Golden Age (1948 to 1973) using a narrative approach, American Economic Journal: Macroeconomics, 6(4), 2014, 137-69). English credit controls (1959-1980) had an effect on bank lending that was different from the effect of interest rates (Aikman, D., ,Bush, O. & Taylor, A. M., Monetary Versus Macroprudential Policies: Causal Impacts of Interest Rates and Credit Controls in the Era of the UK Radcliffe Report, Bank of England staff working paper, 2018). Galati, Kakes & Moessner (2020) study The Dutch central bank experienced ceilings on net credit creation (1960-1991) and banks responded to them by shifting to more long-term funding (Galati, G., Kakes, J., & Moessner, R., “Effects of Credit Restrictions in the Netherlands and Lessons for Macroprudential Policy (No. 679), Netherlands Central Bank, Research Department, 2020.

[15] This section draws on the conclusion of Monnet, E., Controlling Credit, Cambridge University Press, 2018.

[16] On the dangers and virtues of historical analogies in the context of economic policy making, see Eichengreen, B., “Economic history and economic policy”, The Journal of Economic History, 2012, 289-307.

[17] Bordo, M. D., An historical perspective on the quest for financial stability and the monetary policy regime, The Journal of Economic History, 78(2), 2018, 319-357.

[18] Taylor & Schularick, Op.cit., 2012 and Taylor, A. M., The Great Leveraging (No. 9082), CEPR Discussion Papers, 2012.

[19] Tooze, A., Crashed: How a Decade of Financial Crises Changed the World, Penguin, 2018.

[20] Monnet, E., & Puy, D., One Ring to Rule Them All? New Evidence on World Cycles (No. 19/202), International Monetary Fund, 2019.

[21] Monnet, Op. Cit., 2018, Chapters 5 and 7.

[22] Examples from earlier times could also shed a distinct light on this issue. In their study of the relationship between the Bank of England and the English State in the 18th century, Patrick O’Brien and Nuno Palma emphasize – following Adam Smith – that the Bank of England worked as the “great engine of the State”. The Bank helped the state through various ways, either direct financing or the development of a liquid bond market. However, the Bank’s institutional framework (private shareholders and gold standard), even informally, made it clear that central banks could be in a position to refuse advances to the State (which was done on several occasions) and that a balance of power was at play. O’Brien, P. K., & Palma, N., Not an Ordinary Bank but a Great Engine of State: The Bank of England and the British economy, 1694-1844, (No. 20-03), The European Association for Banking and Financial History (EABH), 2020.

Our partners

Sections

Keep in touch

© laviedesidees.fr - Any replication forbidden without the explicit consent of the editors. - Mentions légales - webdesign : Abel Poucet